Thanks to the loosening of certain SEC regulations over the past decade, individual investors now have the ability to invest in many attractive but previously unavailable asset classes. While crowdsourced real estate gets a lot of attention, lesser-known asset classes like private credit have a lot to offer investors as well.

Percent (formally called Cadence) was founded in 2018 to give investors access to the private credit market.

In this Percent review, we’ll cover:

- How the platform works.

- What investments are available.

- The fees Percent charges.

- Alternatives within the private credit space.

Additionally, we’ll analyze the private credit investing market as a whole, to help you determine if Percent is right for you.

Pros

- Provides access to a diversified array of short-term, high-yield investment opportunities.

- Minimums start as low as $500.

- 100% of the investments are backed by assets.

Cons

- Deals on the platform are funded quickly.

- No secondary market to liquidate investments.

How Percent Unlocks Private Credit Investments

Founded in 2018, Percent gives accredited investors exposure to privately negotiated loans and debt financing within the private credit space. The company performs due diligence on different loan originators, then offers its user base a platform to invest in those loans.

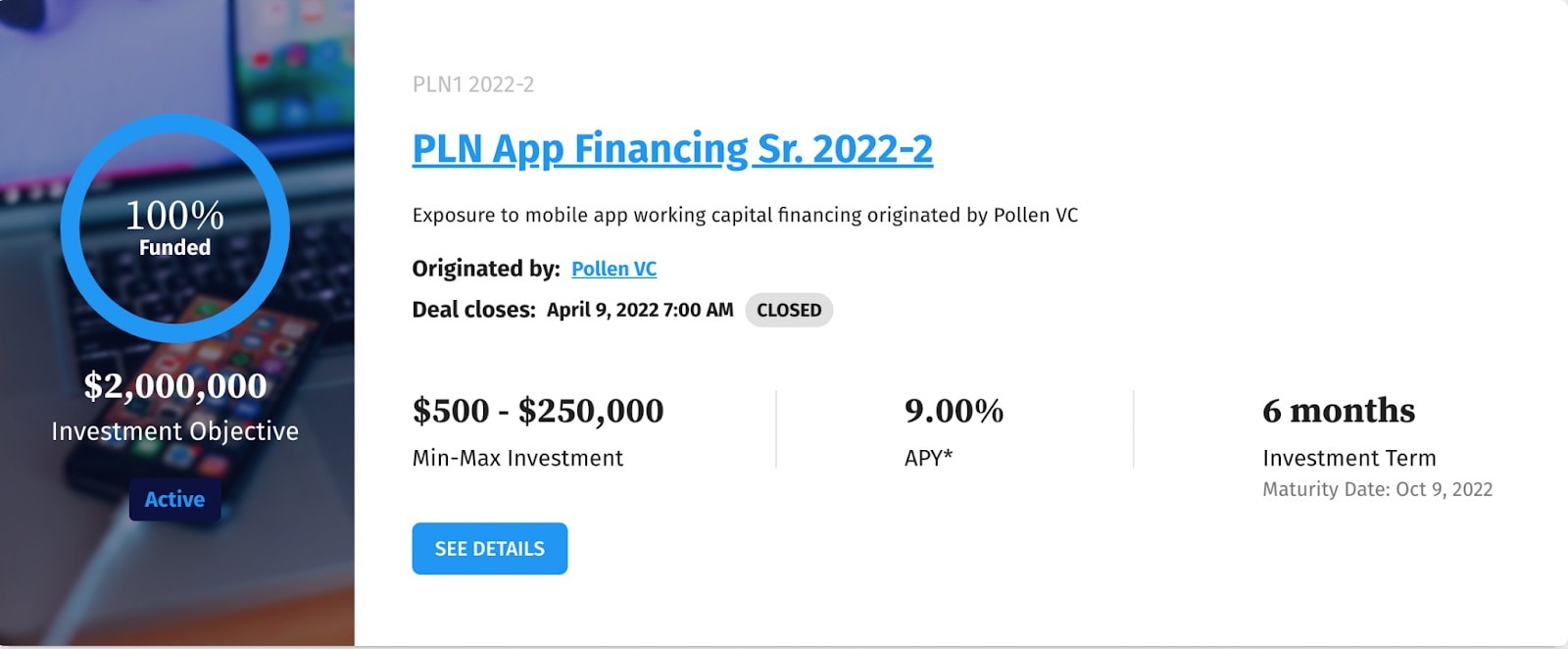

Debt originators specialize in a specific type of loan or debt financing, such as working capital and merchant cash advances. As an investor, you’re investing in a portfolio of these loans or advances from a specific originator.

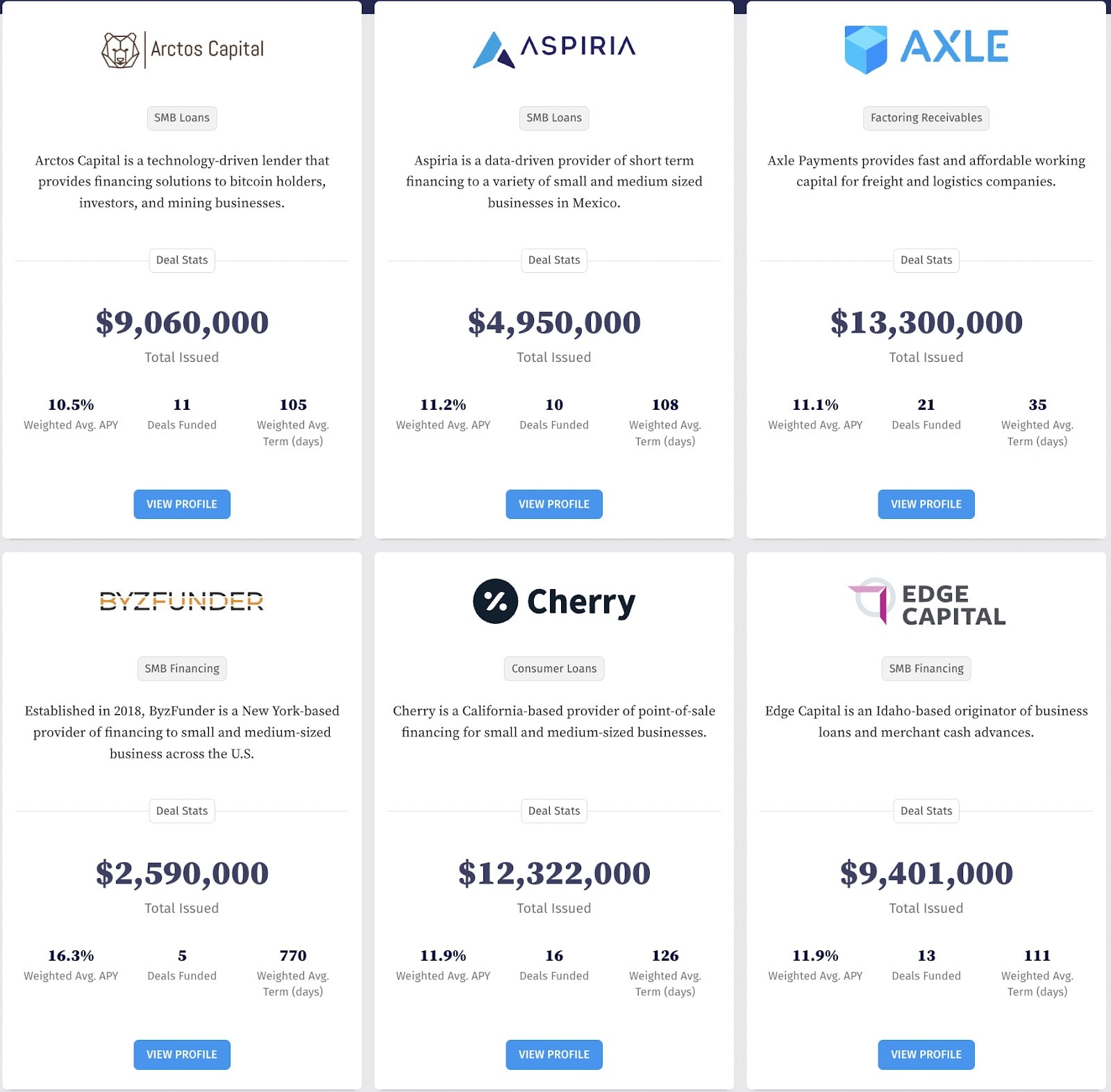

Currently, there are 30 originators on the platform, each specializing in a different type of private credit financing. This allows you to invest in notes offering exposure to residential mortgages, short-term small business loans, merchant cash advances, stablecoin loans secured by cryptocurrencies and more.

A “special purpose vehicle” or SPV is used for each offering. This SPV allows you to invest in the assets specific to that offering, instead of the company as a whole.

While 100% of the offerings on Percent are backed by assets from the individual or corporation receiving the funds, the security you’re purchasing is issued by the SPV itself and is considered an unsecured note. It’s the issuer of the SPV and not the SPV itself that retains secured claims on assets (more on defaults below).

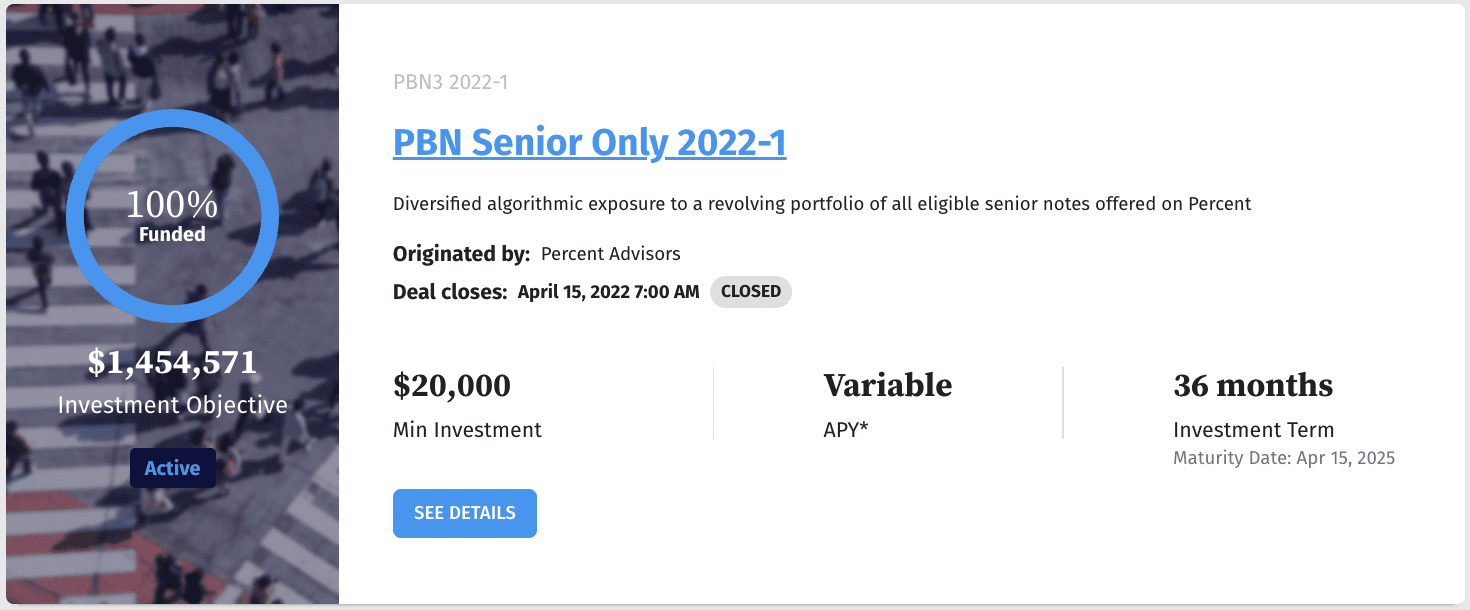

Percent Blended Note

In addition to individual private credit opportunities with a specific loan originator, Percent offers what it calls a Percent Blended Note, which provides investors with exposure to a selection of the private credit offerings on the platform. You can think of it as being similar to a mutual fund.

The idea behind Percent Blended Notes is that they provide built-in diversification of your private credit holdings. Percent discloses the underlying assets for its Blended Note, so you can see what opportunities the note invests in. These notes also provide variable monthly interest and amortization payments to investors.

Percent’s Blended Notes have a $20,000 minimum investment requirement and a 1% management fee.

Percent’s Historical Performance

Between June 2018 and May 10th of 2022, Percent funded 307 deals and earned investors an average weighted APY of 14.38%. In total, they’ve returned $493 million to investors.

Their current default rate is 1.75%. This default rate represents the ratio of principal payments that were not made in full and on time (subject to a five day grace period).

When a borrower gets a loan from an originator listed on Percent, that loan is collateralized and backed by assets. As such, there are protections in place so that an investment never goes to zero.

Percent’s Costs and Fees

In the past, Percent did not charge fees to invest in standard private credit opportunities. Instead, the company generated revenue by charging fees to loan originators for providing capital. But the company plans to roll out a new fee structure in the coming months.

Under this new fee structure, Percent will charge 10% of the stated interest rate on its private credit offerings. In other words, if you receive $500 in interest in a month from one of your investments, Percent will collect $50 from your distributions before they reach your account.

Note that Percent charges additional fees for Percent Blended Notes, which come with a 1% management fee on invested assets.

Using a Self-Directed IRA to Invest With Percent

You can use two types of accounts to invest in Percent’s private credit offerings: taxable accounts and self-directed IRAs (SDIRAs).

A taxable account is the standard type of account you’ll be issued upon signing up for Percent. The company furnishes a 1099-INT form for its taxable account holders each year if they earn income from their investments on the platform.

If you’re interested in investing in private credit opportunities through Percent with a tax-advantaged account, you can do so with a self-directed IRA through Alto. Investing in Percent’s offerings through an Alto IRA has a minimum investment requirement of $2,500. You can learn more about how the platform works in our Alto IRA review.

Percent vs. Yieldstreet

Yieldstreet is another popular alternative investment platform. Like Percent, Yieldstreet connects investors with non-traditional assets, including private credit. But there are a few key differences between these platforms, such as:

- Supported asset classes. The first significant difference is in the types of investing Yieldstreet supports. Overall, Yieldstreet has a broader selection of investment types, while Percent focuses on asset-backed notes.

- Fee structure. Yieldstreet charges an annual management fee on all accounts, which ranges from 0% (for short-term notes) to 3%.

- Self-directed IRA opportunities. Although you can invest in Percent’s offerings through an SDIRA, doing so requires that you have an SDIRA with another provider. Yieldstreet offers its own SDIRA, which you can use to invest in any of the assets on the platform.

- Support for non-accredited investors. The majority of Yieldstreet’s investment opportunities are only open to accredited investors. However, Yieldstreet has a multi-asset fund called the Prism Fund that’s open to non-accredited investors with a $10,000 minimum. This managed fund invests in a mix of opportunities on Yieldstreet’s platform, so it offers non-accredited investors a way to get exposure to some of these alternative assets.

- Historical returns and total number of investments. Yieldstreet has historically lower returns than Percent (around 9% compared to Percent’s 14%). But Yieldstreet is a much larger platform with more than $2.5 billion invested to date.

Percent and Yieldstreet are both interesting options for people who want access to private credit investing opportunities.

Yieldstreet has an advantage over Percent when it comes to its diversity of asset classes, built-in SDIRA support, and opportunities for non-accredited investors. But Yieldstreet’s higher-fee structure and its lower historical rates of return are worth considering before you sign up.

Learn more about the platform in our Yieldstreet review.

Platforms that enable you to increase in real estate debt, include:

- Fundrise: Specializes in a variety of real estate debt investments, including senior debt loans and mezzanine loans, through its eREITs. See our Fundrise review.

- EquityMultiple: Offers investors opportunities in first position mortgage loans and subordinated debt, focusing on commercial real estate. See our EquityMultiple review.

- CrowdStreet: Provides access to direct senior secured loans, bridge loans, and construction loans, targeting commercial real estate projects. See our CrowdStreet review.

Percent Investing: Our Take

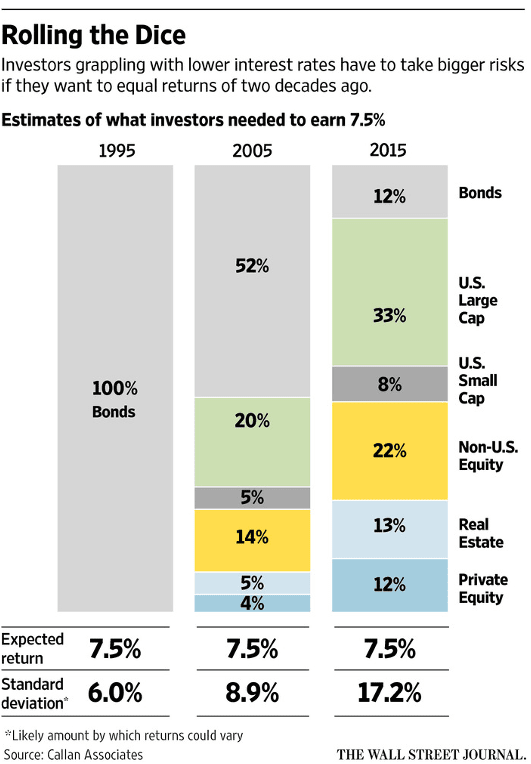

Individual investors’ strategies often lag behind the strategies used by pension funds. In 2016, the Wall Street Journal published a fascinating report on how pension funds have shifted their strategy over time, not in an effort to increase returns but simply to maintain them.

You can see this strategy shift in the graphic below:

Private credit investing falls within the more aggressive approach that pension funds started taking a while back.

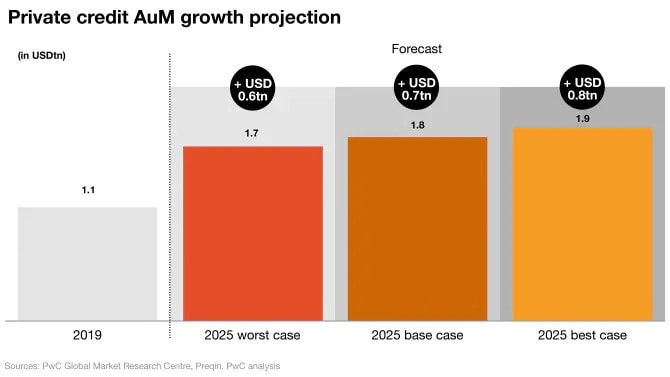

Individual investors have followed pension funds in that same search for yield. Alternative investments are expected to go from 12% of the global financial market in 2018 to as high as 24% in 2024. Non-bank lending is also a growing trend, with an expected increase from $1.1 trillion in 2019 to $1.8 trillion in 2025.

This is why it’s encouraging to see a company like Percent provide a simplified way for accredited investors to add private credit to their portfolios.

As a platform itself, there’s a lot to appreciate about Percent, including its solid track record, its modest investment minimums, and its reasonably low rate of default.

However, it’s not a platform I would suggest to a novice investor. As you’re often investing in specific types of loans, it’s important that you understand the risk and reward of each particular asset class.

Percent is also best for investors who have the funds needed to diversify into multiple asset classes on the platform, or who have the minimum funds required to invest in a Percent Blended Note.

While deals are listed frequently on the platform, they do tend to fill up fast. As such, it can take some time to round out your portfolio with your desired diversification.

Disclosure: I am a paid partner of Yieldstreet, a company that operates an online investment platform, and have been compensated for referring investors to Yieldstreet investments. This financial relationship may influence the content, topics or posts made on this platform. The views and opinions expressed on this platform are purely my own. This content is not intended to provide investment advice. Investing involves risk, including loss of principal. Please carefully review Yieldstreet’s Offering Circular before making any investment.

Thank you so much for writing this extremely informative article! I googled for reviews on Percent.com as I was having trouble on their site researching the offers and trying to get an idea of risks, benefits, how to best mix investments! This was a nicely concise and full of helpful information to guide my path! I’m intrigued by alternative investments as I seek better yields than typical fixed income, yet not taking on crazy risk!

I will now check out the content on the whole site! Thanks again!

Paul

Thank you, Paul, for the kind words. Glad you found the content helpful.